(Michael Sedacca, Rareview Capital) Quantitatively, there is the most fear priced into the municipal-bond closed-end fund sector in over a decade. If you own and plan to hold municipal bond closed-end funds over the medium-term, based on the relative value to municipal cash bonds, there is a compelling argument you should not sell them. Moreover, leading up to the first interest rate hike by the Federal Reserve in the coming weeks, there is a strong case that an allocation should be made to this sector.

(Want to see how Rareview does it? Check out their models.)

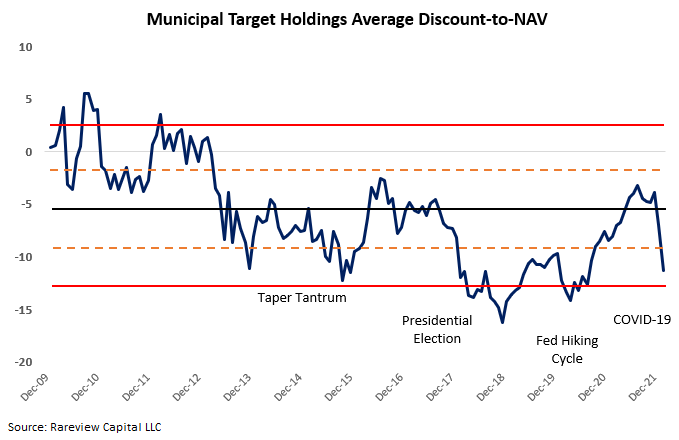

MUNICIPAL BOND CEF DISCOUNTS-TO-NAV

Municipal bond closed-end funds (“CEFs”) make up approximately one-third of all CEFs – they are the largest sector by far. Mechanically, their discount-to-NAV widens or narrows based on the change in their distribution yield. The largest marginal input in determining the distribution yield is the change in leverage costs. When leverage costs rise because of higher short-term borrowing rates, the distribution rate falls, and the discount-to-NAV widens. Conversely, when leverage costs fall because of lower short-term borrowing rates, the distribution rate rises, and the discount-to-NAV narrows. Therefore, municipal bond CEF discounts-to-NAV is the most straightforward to quantify of any fixed income sector because changes in interest rates explain ~99% of all movements in broad municipal bonds over the intermediate-term.

Occasionally, those discounts can widen in the short-term based on a high degree of fear in the marketplace. As a result of the fixed income market now pricing in 7-8 interest rate hikes in 2022, up from 3-4 hikes on December 31, 2021, we believe this is one of those times.

In response, municipal-bond CEF discounts in our target universe have widened to -11.30% from -3.88% on December 31, 2021. This -7.42% discount widening in the past six weeks is the fastest rate of change since the Great Financial Crisis.

A z-score is a measure of how far an asset has moved from the mean. Statistically, on a scale of +2.0 to -2.0, the absolute level of discounts has fallen from +0.6 to -1.7 z-score scores. To further put this in context, discount-to-NAV’s are in the 95%-percentile of cheapness.

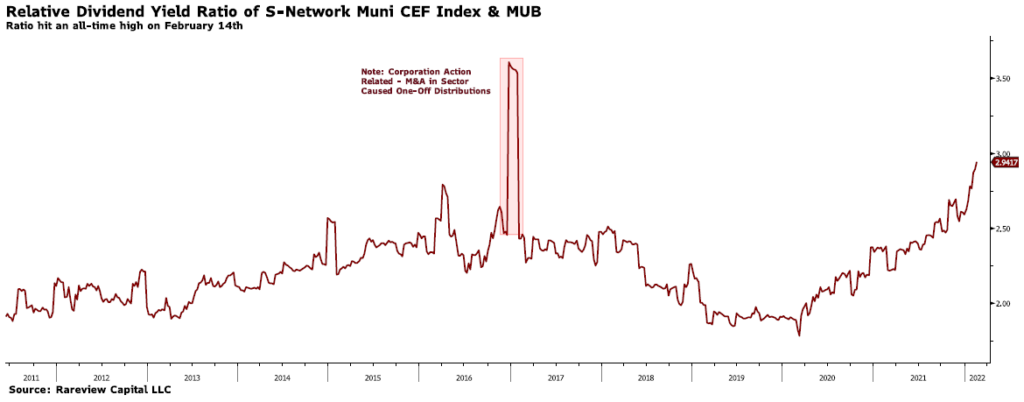

DIVIDEND RATIO: MUNICIPAL BOND CEFS VS. CASH MUNICIPAL BONDS

In addition to analyzing discounts-to-NAV’s to measure the historical cheapness of the sector, we compare the annualized distribution yield of municipal bond CEFs to cash municipal bonds. The proxies we use are the S-Network Municipal Bond CEF Index (symbol: CEFMX) and the iShares National Muni Bond ETF (symbol: MUB).

The latest annualized distribution yield for CEFMX is 4.98% relative to MUB’s 1.69%, or 2.95 times greater.

Historically, this relative dividend ratio is 2.20-2.25 times greater than municipal cash bonds. Currently, at 2.95 times, this is the highest relative dividend ratio since the inception of the CEFMX Index! Said differently, the key determinant for owning municipal bond CEF’s during a Fed tightening cycle – their relative dividend yield – has the most attractive starting point since the Great Financial Crisis.

Note that at the end of the 2018 hiking cycle, when the yield curve inverted, the ratio fell below 2.0. The critical point is that even if the spread between funding and investment rates narrows, and the absolute dividend-per-share in municipal CEF’s declines, the ratio has a significant head-start if the Federal Reserve undertakes an aggressive interest rate hiking cycle.

MUNICIPAL BOND CEF DISTRIBUTIONS

As leverage costs rise, municipal bond CEF’s mechanically cut their distribution rates in-kind as stated above. Typically, distribution cuts in the municipal bond CEF sector are approximately 15% during a Fed hiking cycle. For example, if the monthly distribution for a municipal bond CEF were $0.07/share, it would decline to ~$0.06/share.

Today, for the CEFMX/MUB ratio to revert to its historical range, the average municipal bond CEF would need to cut its dividend by ~24.5%. This is substantially more than the normal ~15% distribution cuts over a Fed tightening cycle for the municipal bond CEF sector.

CONCLUSION

Quantitatively, there is the most fear priced into the municipal-bond closed-end fund sector in over a decade. If you own and plan to hold municipal bond closed-end funds over the medium-term, based on the relative value to municipal cash bonds, there is a compelling argument you should not sell them. Moreover, leading up to the first interest rate hike by the Federal Reserve in the coming weeks, there is a strong case that an allocation should be made to this sector.

Rareview Capital LLC is a registered investment adviser and ETF sponsor. We build goals-based investment management strategies that can be accessed through ETFs, sub-advisory/dual contract, model portfolios, or by opening an account directly with us.

If you have any questions or would like to hear more about our ETFs, please reach out.

DISCLAIMER

This material is for informational purposes only and does not constitute an offer or a solicitation to buy, hold, or sell an interest in any investment or any other security, including any investment with Rareview Capital LLC (“RVC”) or any of its affiliates or any other related investment advisory services. This material is not designed to cover every aspect of the relevant markets and is not intended to be used as a general guide to investing or as a source of any specific investment recommendation. This material does not constitute legal, tax, or investment advice, nor is it a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional adviser. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice. In preparing this material, RVC has relied upon data supplied by third parties. RVC does not undertake any obligation to update the information contained herein in light of later circumstances or events. RVC does not represent the information herein is accurate, true or complete, makes no warranty, express or implied, regarding the information herein, and shall not be liable for any losses, damages, costs or expenses relating to its adequacy, accuracy, truth, completeness or use. This material is subject to a more complete description and does not contain all of the information necessary to make any investment decision, including, but not limited to, the risks, fees and investment strategies of an investment. All investments carry a certain degree of risk, including the possible loss of principal. There is no assurance that an investment will provide positive performance over any period of time. There are specific risks that apply to investment strategies. Closed-end funds frequently trade at a discount to their net asset value. These risks should be reviewed carefully before taking any investment action. Since no one investment style or manager is suitable for all types of investors, this site is provided for informational purposes only. The statements contained herein are the opinions of RVC. This site contains no investment advice or recommendations. Individual investor results will vary. Rareview Capital LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing. Past performance is no guarantee of future results.