A factor focus can be an excellent strategy for advisors seeking to differentiate themselves to their clients.

For example, some clients may be familiar with some but not all of the important investment factors. Likewise, many clients may not be aware that factor leadership is rarely stagnant and can change from year to year.

WisdomTree’s series of model portfolios assist advisors in delivering much-needed factor diversification, ensuring client portfolios aren’t overly dependent on a single factor and are adequately positioned to capitalize on shifting factor-level trends.

Why Model Portfolios Are Important for Factor Allocations

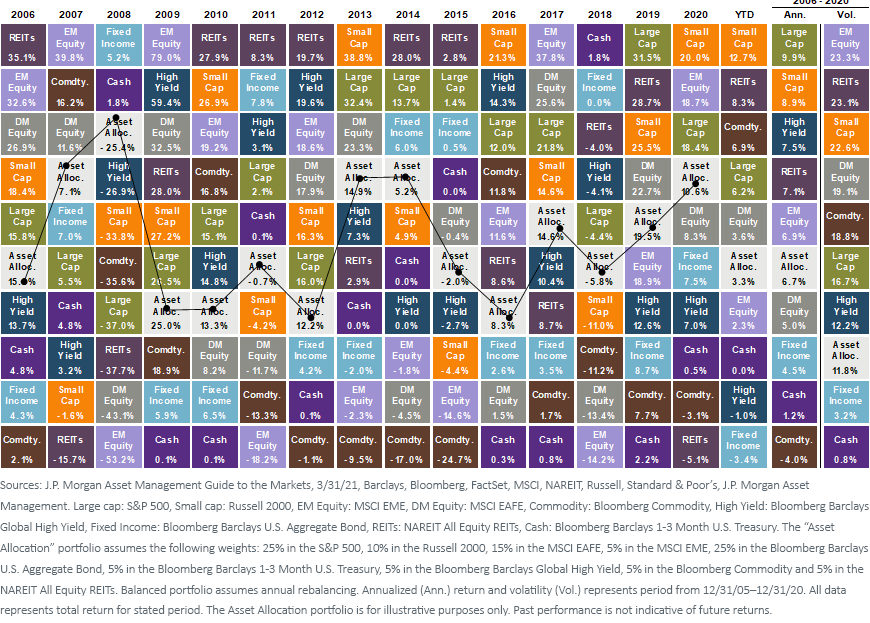

The example of rotating asset classes paints the picture of why factor diversification is relevant to clients. In the 15-year period spanning 2006 through 2020 there were just two examples of one year’s leading asset class maintaining that perch in the following year. Real estate investment trusts (REITs) led from 2010 through 2012 and again in 2014 and 2015, according to WisdomTree research.

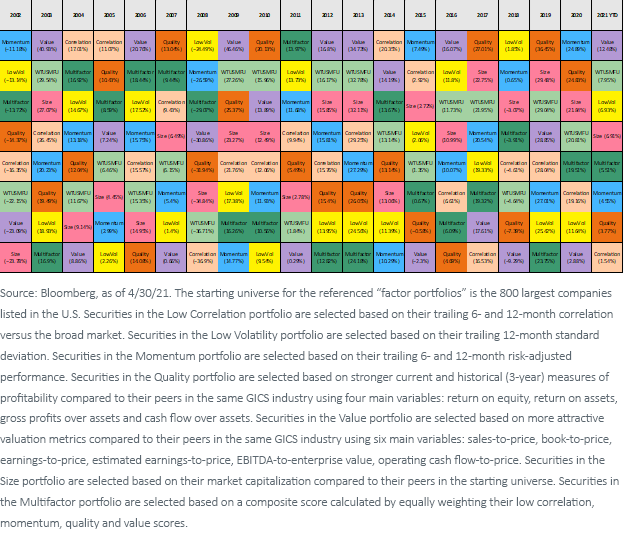

That’s a point worth remembering with factors because a similar scenario played out over the same period. From 2002 through 2020, there were just two examples of one year’s best-performing factor maintaining that dominance the following year: correlation in 2004 and 2005 and value in 2012 and 2013.

As WisdomTree Chief Investment Officer – Model Portfolios Scott Welch points out, the past year of factor action underscores the importance of diversification.

Previously, it was “all growth and momentum, all the time. Value, quality and dividends were in the caboose of the train,” he said in a recent note. “Compare that to the past 12 months. It appears dividends and value have driven performance, while growth and momentum have moved to the rear of the bus.”

Point is factor selection is just as tricky as picking among asset classes or individual securities. Advisors don’t know when factor leadership will shift, highlighting the benefits of staying diversified in advance of changes atop the factor leader board.

“The point we’re trying to make is that it is just as difficult to predict factor rotation as it is asset class rotation,” concludes Welch. “We’re not sure anyone predicted the massive factor rotation back toward small caps and value that occurred after the Pfizer vaccine announcement came out last November (though, given that many WisdomTree products have a value or size ’tilt’ to them, we certainly have enjoyed it). Value stocks in particular have roared back.”

This article originally appeared on ETF Trends.

{kind=link}

{kind=link}