(Flexible Plan / David Wismer)

Barron’s noted in late May that “Signs of economic weakness are piling up …,” and The Wall Street Journal summarized in an analysis on June 5, “Overall, the data has clouded some asset managers’ outlook of the U.S. economy.” (See this recent article in Proactive Advisor Magazine for a recap of these findings.)

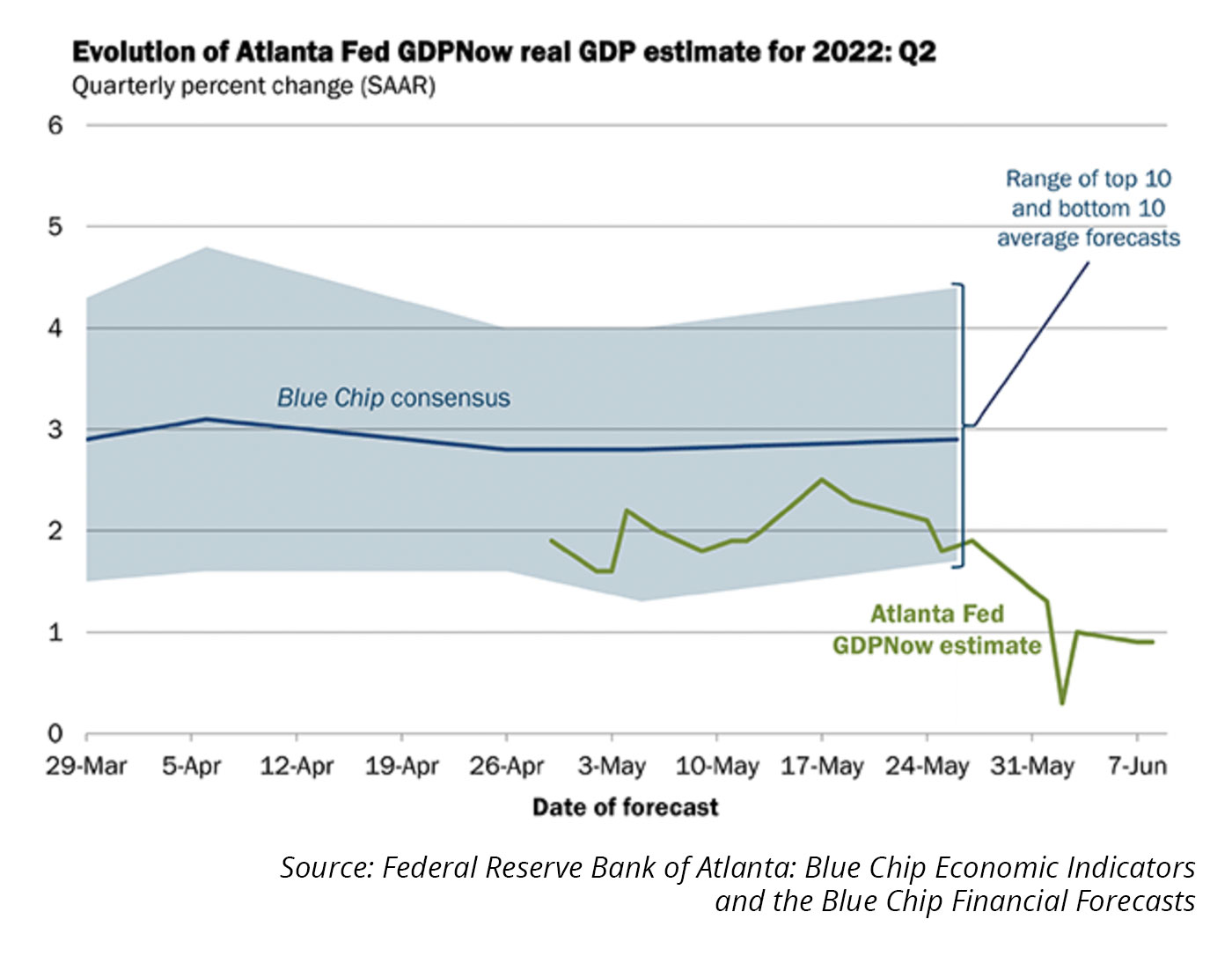

While forecasts from the Atlanta Federal Reserve on GDP growth are often discounted, they are nonetheless followed closely by Wall Street.

In the June 8 GDPNow tracker from the Atlanta Fed (before the most recent CPI data), the estimate for Q2 2002 growth continued to move lower since mid-May and is now estimated at 0.9%.

Following the CPI report, Barron’s “Up and Down Wall Street” column featured a very blunt view of the market impact:

“… Inflation is too high, which means interest rates are too low. And while price/earnings ratios have come down to reflect the rise in rates to date, earnings expectations underlying P/E calculations have not adjusted appreciably. The product of lower P/E multiples and lower earnings forecasts is lower stock prices.”

Financial advisers’ holistic approach to risk management

As the editor of Proactive Advisor Magazine, one theme I hear consistently is how financial advisers believe that a major component of their role, and one where they add great value, is in helping clients preserve, protect, and grow their wealth using a variety of risk-management strategies.

This is particularly relevant in an inflationary environment—both for the short and long term.

While we typically think of risk management in the context of investment portfolios, these advisers take a broad and holistic view of strategies they can use to help clients protect their assets, their lifestyle, and the future needs of their families. These might include insurance strategies in a variety of areas, legacy and beneficiary planning, tax-mitigation strategies, health-care and long-term-care planning, business-succession planning, retirement-income planning, and cash-flow management.

That said, risk management and wealth preservation related to investment planning are major components of what these advisers do. A tremendous amount of time is devoted to understanding the qualitative, emotional, and behavioral side of how their clients view risk. Advisers then employ more objective and quantitative tools to assess a client’s risk profile, trying to differentiate between a client’s stated risk appetite, their actual risk capacity, and “what the numbers say.”

Many advisers I interview say most clients have assumed too much investment risk before they come to work with the adviser, are unaware of how much risk they really have in their portfolios, and are too focused on short-term returns rather than long-term objectives and goals. Education on these types of issues becomes a major focal point in the early stages of the client-adviser relationship—a sound practice that should lead to more positive and satisfactory outcomes in the long run for clients.

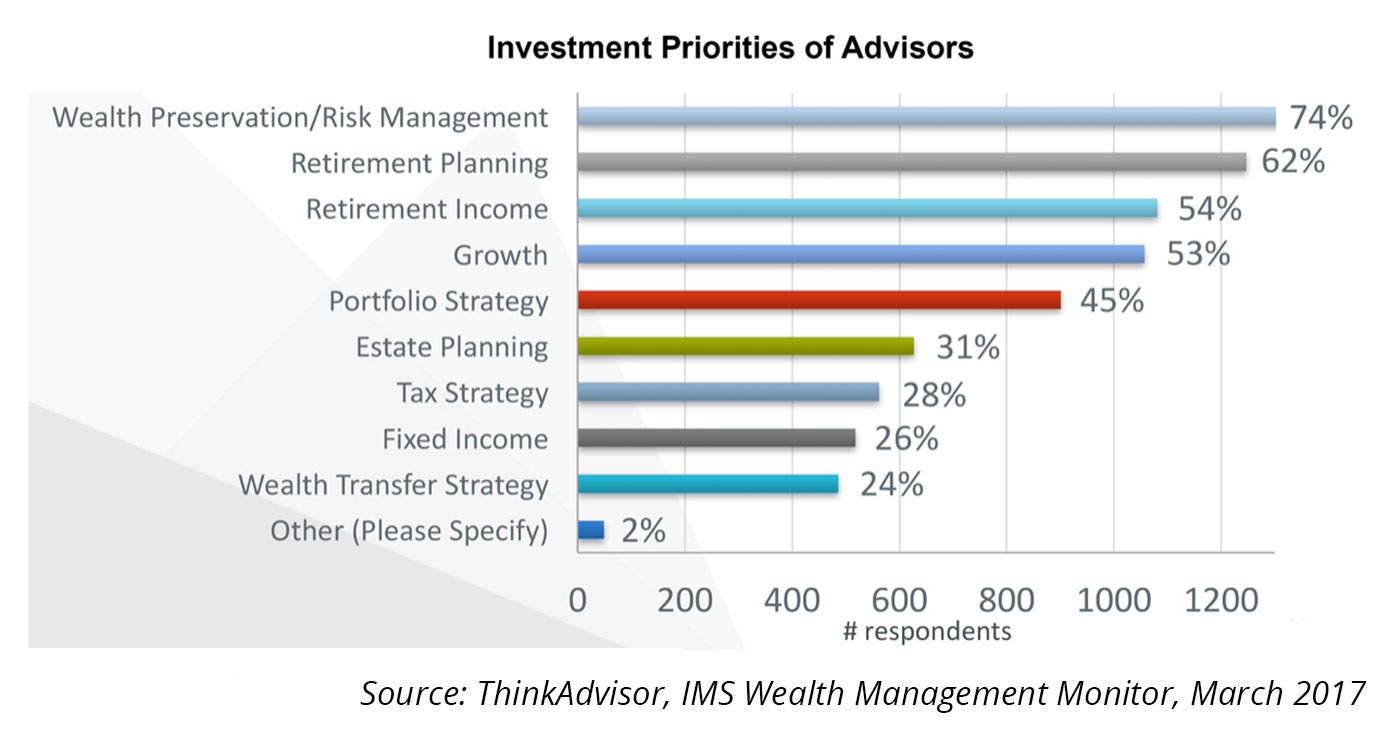

A comprehensive study of financial advisers and affluent clients by IMS Wealth Management Monitor (summarized by ThinkAdvisor) reinforced the fact that “the number one investment priority for 74% of asset managers surveyed … is wealth preservation and risk management.”

Many advisers I have interviewed turn to the investment management offerings of Flexible Plan Investments (FPI) for a role in their client portfolio allocations.

For over 40 years, FPI has been dedicated to preserving and growing wealth through dynamic risk management, with strategies built to perform through full market cycles. This emphasis on strategies that mitigate volatility is appealing to advisers dedicated to their clients’ objectives of building a comprehensive investment plan that can deliver long-term competitive performance, while attempting to minimize losses in down market periods. Advisers are also attracted to the sophisticated, rules-based, quantitative nature of FPI’s strategy offerings, which helps to take emotion and manager discretion out of the investing equation.

One adviser I interviewed had an interesting example he uses with clients to describe this type of active portfolio management:

“I like to use an analogy with clients related to advances in automotive technology. I ask them if they would rather be taking a long trip on busy highways in a Model T, which has essentially two gauges, one for fuel and a speedometer. Or would they rather take that trip in a Tesla, which has not only all of the most modern safety features and incredible fuel efficiency, but also active driver warning systems, easy access to GPS technology and traffic alerts, and the latest driver technology in every regard. Which vehicle do they think is going to provide a more comfortable, safer, and more interactive driving experience that can avoid the many types of hazards one faces on the road today?

“The same concept is true for their investment portfolio. We use managers who employ strategies that are computer- and algorithm-driven and modern in every sense of today’s investment world. They have advanced indicators and trend-following techniques that seek to keep a portfolio out of harm’s way. Our educational process concerning this sophisticated approach to portfolio management is very important to our practice and our clients. I think it is a core differentiator for our firm and helps drive high levels of satisfaction with our overall approach to wealth management.”

***

Many financial advisers we interview emphasize to clients that risk management—investment or otherwise—is not something that should be considered only when trouble is looming on the horizon. Complacency, they say, can be their clients’ worst enemy. Risk management should be consistently incorporated throughout a customized investment plan from its inception, with a portfolio including risk-managed strategies built to react proactively to changes in market conditions.

That is a message that FPI has always embraced.