by Michael Sedacca, Rareview Portfolio Manager

Seasonality is the tendency for securities to perform better during some periods and worse during others.

In the last quarter of the year, closed-end funds (“CEF’s”) tend to have seasonally weak performance. Specifically, between November 1st and December 15th, CEF performance on average is negative relative to the underlying assets. While we cannot quantify the precise reason, we believe the most likely cause is tax-loss selling.

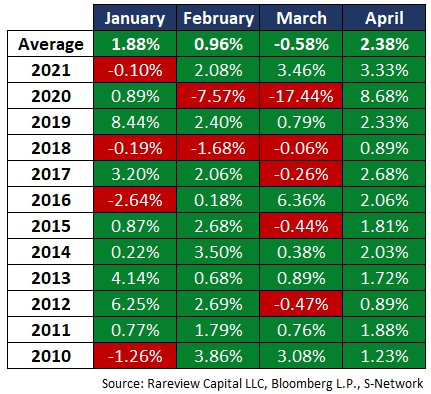

Conversely, CEF‘s have strong positive seasonality in the first four months of the year. Specifically, between January 1st and April 30th, the S-Network CEF Index (CEFXTR) gained in 9 of the last 11 years. The average gain during the four months was 4.64%. Also, the month of April was positive for all 11 years. Note that the only two years of declines had catalysts. In 2018, the market was in the teeth of the Federal Reserve (“Fed”) hiking cycle, and in 2020, the pandemic.

The seasonality is playing out again this year, especially for fixed income CEFs, which make up two–thirds of all CE’s. Drilling down further, price returns are most negative for fixed-income CEF sectors sensitive to a rise in short-term interest rates.

The average discount-to-NAV for the universe of fixed income CEFs that we track has widened from -5.91% at the end of September to -9.41% today, or -3.50%. As a yardstick, fixed income CEF discounts-to-NAV oscillate between a range of -5% and -10%. So, currently, at near -10%, the discount-to-NAV is at the very wide end of the historical range.

We believe the current setup is an opportunity to potentially capture the positive CEF alpha that may be generated through the end of April.

If you are interested in learning more about how we use closed-end funds to construct portfolios, please call us at 212-475-8664 or email us at info@rareviewcapital.com.