(Forbes) Stocks and bonds yield 2% these days. That’s problematic if you had in mind withdrawing 4% a year from your savings. Wall Street’s answer to this predicament: a rich menu of exchange-traded funds with high yields.

Here I will highlight the best funds in seven different investing styles that deliver outsized payouts. Among them: funds that own junk bonds, funds that invest in pipeline partnerships and funds that own European stocks.

I see these funds as useful even for investors who are not seeking current income. They offer diversification. They don’t behave exactly like either the high-grade bond funds or the S&P 500 funds that probably account for the bulk of your savings.

But before you dive in, ponder two things. One is that handsome yields always come with a cost in either higher risk or diminished growth. No dividend is a free lunch.

The other matter is that distributions aren’t the only way to get cash to live on. You could always sell a few shares of a fund. You could, that is, skip the yield chase and instead put your money in something more conventional, like the Vanguard Balanced Index Fund. When that yields 2%, you’d get the rest of a 4% spending target by liquidating 2% of your shares every year.

If selling shares isn’t to your liking—or you just want to diversify into categories not well covered with a plain old balanced fund—then look at portfolios containing these yield-spewing securities.

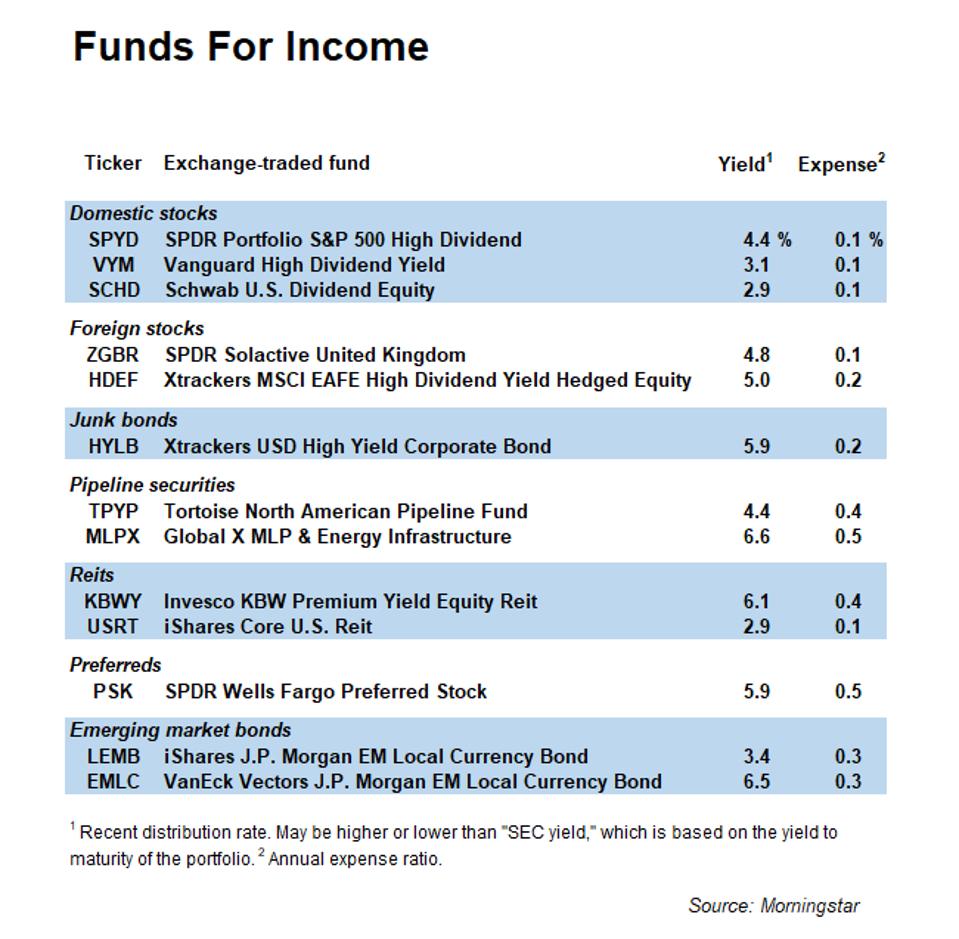

1. High-yield domestic stocks

Numerous ETFs aim at big-company stocks with yields higher than average. Some of them charge minuscule fees, and you can find the bargains in the Best ETFs for Investors: Dividend Funds report.

You’ll find Vanguard High Dividend Yield and Schwab U.S. Dividend Equity at the top of this cost efficiency ranking. They both yield 3%, more or less, and they both emphasize blue chips like Exxon Mobil and Verizon Communications.

You can reach out a little further for yield. The SPDR Portfolio S&P 500 High Dividend ETF from State Street, whose fees are a tad higher, has pushed its yield well above 4%. It owns the likes of Newell Brands and Nordstrom.

What did we say about yield coming with higher risk or lower growth? Newell can scarcely be said to be covering its generous dividend; it’s in the red. Nordstrom is making good money, but it’s in a dying industry.

If you want equities that pay fat dividends, you can get them. Just know what you’re getting.

2. High-yield overseas stocks

It’s easy to put together a collection of foreign stocks with nice yields because dividend paying is more of a habit outside the U.S., especially in Europe. The Xtrackers MSCI EAFE High Dividend Yield Hedged Equity ETF yields 4.7%, net of fund fees (an affordable 0.2%). Holdings include Total, the French oil company; Zurich Insurance Group, known here as Farmers Insurance; and Japan Tobacco.

Slightly cheaper and considerably narrower: State Street’s SPDR Solactive United Kingdom, with an expense ratio of 0.14%. Its largest positions are in HSBC, the bank, and BP, the oil company.

As always, high yield = low growth. The European economy is sleepier than ours. Also, European companies tend to spend less than American ones on stock buybacks. A buyback is like a reinvested dividend, trading today’s cash for tomorrow’s price appreciation.

Euro funds belong in a taxable account, where you can claim a credit for the foreign taxes withheld from your dividends. In an IRA the foreign taxes don’t do as much good: They simply reduce the taxable income you will someday pull out of the account.

3. Junk bonds

IOUs from shaky companies pay high interest to make up for the fact that some of those borrowers won’t pay you back. In the Forbes ranking of cost-effective junk bond ETFs, Xtrackers USD High Yield Corporate Bond is the winner. It’s on our ETF Honor Roll.

The Xtrackers junk fund has a yield of 5.9%, reports Morningstar. I like this fund. But don’t be deluded about what you’re going to get from it.

That reported yield is calculated before subtracting bad debt losses, which might average 1% to 2% a year over a full economic cycle. Subtract another 1% to 2% for inflation. Now subtract something for the adverse selection in this business: Good borrowers prepay their bonds, cheating you out of those high coupons. Your portfolio becomes concentrated in loans to weak borrowers.

What’s the likely real return on a junk portfolio? Somewhere around 2%.

Spend the whole 5.9% if you want to. But understand what you’re doing. You’re spending a real return of 2% and then liquidating your principal at a rate of 3.9%. You won’t notice this principal erosion every year—especially not if the economy is booming and inflation tame—but you will see it over time.

4. Pipeline securities

Partnerships and corporations that own oil and gas pipelines gush out fat distributions. You can own pieces of these things via exchange-traded funds.

Two ETFs I like are Tortoise North American Pipeline and Global X MLP & Energy Infrastructure. They both have portfolios mixing the units of master limited partnerships with the shares of corporations. They both have fairly modest yields, in the range of 4% to 6%.

Two cautions apply. One is that transporting fossil fuel has an even more questionable future than does running a department store. Someday the carbon will be displaced. Not soon, but it will happen, and when it does, you’ll own buried scrap metal.

The other, more subtle, problem is that many pipeline ETFs reach for yield by loading up on partnerships (like Plains All American Pipeline), as opposed to corporations (like Oneok). The partnerships tend to have nicer payouts, in part because they owe no corporate income tax. But if a fund has more than 25% of its portfolio in partnerships, it has to allow for corporate income tax on the fund itself.

When partnership units fare badly in the stock market, as they have done in recent years, the future tax liability doesn’t have any impact on the fund’s performance. But when the sector rebounds—and presumably you’re investing with that expectation—the fund’s tax bill will hit you in the form of a savagely high expense ratio. I explain the problem and list the funds to avoid in Tax Guide to MLP Funds.

5. Reits

Real estate investment trusts—more precisely, the subset that call themselves “equity” Reits—rent out office buildings, strip malls, apartments and other kinds of property, and pay fairly good dividends out of that revenue stream. An ETF is an excellent way to get your hands on this income.

As always, you have a trade-off between growth and income. The iShares Core U.S. Reit ETF is my favorite among growth-tilting Reit funds. It owns classy Reits like Equinix (data centers) and Prologis (warehouses for e-commerce). It yields just under 3%. It wins the cost efficiency competition detailed in our Best ETFs: Sector Funds review.

For a higher current payout, use the Invesco KBW Premium Yield Equity Reit ETF. It owns weaker companies with fatter dividends, like Washington Prime Group (shopping centers). Its yield tops 6%. Fund fees are considerably higher than on the iShares product.

6. Preferred stocks

With straight preferreds, which are the main offering in preferred-stock ETFs, you get a dividend yield double or more what you might have had on common shares. In return for that, you give up any prospect of growth.

Preferred stocks of good companies act much like junk bonds of bad companies: They couple high current income with the occasional loss of principal. The loss comes when a bond defaults or a preferred suspends its dividend. There are also nicks to principal when a security bought at a premium price gets called in at par.

These capital fluctuations go in one direction. There are no windfall gains from good companies to make up for the windfall losses on bad ones.

The best buy in this category is the SPDR Wells Fargo Preferred Stock ETF. It offsets half its 0.45% expense ratio with income from securities lending. The payout yield has recently been close to 6%, although allowing for the early calls would knock a percentage point off that number.

7. Bonds from junk countries

You can get a nice coupon on sovereign bonds from “emerging” countries, especially if the borrower is planning to repay you in its own iffy currency. My choices in this category are from the BlackRockiShares and VanEck Vectors families, both with J.P. Morgan Emerging Markets Local Currency Bond ETF in the label.

These competing products carry the same 0.3% annual expense burden. They differ in their recent payout rates (3.4% and 6.5%, respectively) but have similar holdings with similar yields to maturity of the bonds. Largest allocations are to Brazil, Indonesia, Mexico, Thailand and South Africa.

You can get hosed if a borrower either devalues its currency or decides that lenders are undeserving of repayment. Indeed, despite nice yields the funds have delivered five-year total returns below 1% a year.

Maybe better times are ahead. In their recent 2020 market outlook, the experts at the BlackRock Investment Institute called out emerging market local-currency debt as due for outperformance. Their call is predicated on a continuation of the dovish monetary policies now in place in developed economies. They are offering no guarantee they will be right.